Introduction – The Hidden Risk Behind Core Banking Transformation

The global banking industry is in the midst of one of its biggest upheavals since the arrival of the internet. Driven by regulatory mandates, the relentless march of digital technology and rising customer expectations, financial institutions everywhere are modernising their core platforms. For large incumbent banks, these programmes can span multiple years and billions of pounds. Challenger banks and fintechs, meanwhile, build their business models on flexible, cloud‑native architectures from day one.

Yet beneath the excitement of launching new digital services lies a quieter reality: data migration is the single most dangerous phase of any core transformation. It is rarely celebrated in board presentations. Customers never see it. Investors hardly ask about it. But those of us who have been in the trenches know that a poorly managed migration can derail even the best funded, best architected programme. When data is corrupted or lost, core banking functions stop. Compliance obligations are breached. Customer trust evaporates. The risks are existential.

This is not conjecture; it’s borne out of experience. For example, mismanaging migration can derail even the most well‑funded, well‑architected transformation initiative. At Ennovision, we have seen banks commit wholeheartedly to new cloud cores, only to find that their largest hurdle lies not in building the target platform, but in moving decades of information from monoliths and mainframes into modern, API‑enabled systems. In other words, you cannot run a digital bank without accurate, governed and accessible data.

This article unpacks why data migration remains such a bottleneck, how automation and AI change the game, and what lessons we’ve learned from global transformation programmes. It is designed for technology leaders in banking, risk officers, project sponsors and product managers seeking to de‑risk their transformation programmes. Throughout, we reference our own platform, CoreAI Integrate, because we believe specialised tooling is essential to making migration safe and repeatable.

Digital Transformation Is Mandatory – But Risk Still Persists

A Worldwide Mandate to Modernise

The reasons behind core banking modernisation are plentiful. Regulators continue to tighten risk reporting requirements, demanding real‑time data aggregation and standardisation. Customers expect instant account opening, real‑time payments and personalised services accessible from any device. Competition is no longer limited to traditional banks; big tech and fintech disruptors have raised the bar on user experience and innovation.

For established banks, the answer is a multi‑year transformation programme that replaces decades‑old technology with flexible cloud‑native platforms. According to industry research, most banks are now actively modernising their core systems due to regulatory compliance, customer expectations, cloud mandates and competitive pressure. These are not minor upgrades; they entail replacing monolithic architecture with microservices, rewriting core processes and enabling open banking APIs. The goals are clear: accelerate time‑to‑market for new products, enable real‑time customer experiences, improve data‑driven decision making and meet regulatory reporting expectations with precision. The impetus to transform is no longer optional.

Why Migration Is the First and Most Underestimated Hurdle

Despite this urgency, the very first hurdle on the road to modernisation is often underestimated: migrating legacy data into the new digital core. Most banks operate dozens of systems built over decades — core banking, customer relationship management (CRM), loan origination, payments, card processing and more. Each uses a different data model, format and taxonomy. Bringing them together into a unified core is a massive undertaking.

The risks of mismanaging migration cannot be overstated. Legacy banking platforms are poorly structured for today’s demands; the data is often fragmented, inconsistent, poorly governed, and buried in systems not designed for cloud or API‑based access. Unless this data is migrated correctly, the modern core cannot function as intended. To make matters worse, banks must maintain operational continuity during migration, ensuring there is no customer disruption. This balancing act is where many programmes stumble.

Beyond Technology: The Human and Regulatory Dimensions

It’s tempting to see migration purely as a technical exercise. In reality, it’s a governance and risk challenge. Regulators scrutinise how banks handle customer data, emphasising data quality, lineage, privacy and compliance. Internal stakeholders need assurances that account balances, transaction histories and customer profiles will be transferred without error. Change management is equally critical: employees who have worked on legacy systems for decades must learn new processes and technologies. If not managed carefully, these human factors can create project‑killing delays.

From an operational perspective, banks must decide whether to migrate via a “big bang” cutover or in phases. A big bang promises faster completion but carries enormous risk if issues surface after go‑live. A phased approach reduces risk but requires complex synchronisation between old and new systems. Without robust automation, both strategies demand armies of developers and testers writing bespoke scripts, reconciling mismatches and manually validating every transaction.

The Data Migration Bottleneck – Complexity and Risk Factors

Disparate Systems and Fragmented Data

One of the most common pitfalls in banking transformation is underestimating how many disparate systems feed the core banking platform. Core banking, CRM, loan origination, payments and other systems each use different formats, taxonomies and business rules. These mismatches create serious integration challenges. Data may refer to the same customer or transaction in different ways, requiring reconciliation. Even basic metadata like date formats, currency codes or address fields can vary wildly across systems.

Because many legacy systems were built as stand‑alone applications, they were never designed for real‑time data exchange or cloud integration. Data is often extracted via brittle nightly batches, stored in flat files or sent through proprietary messaging protocols. Without a unifying data model, mapping fields from source to target becomes a manual, error‑prone process. This complexity is one reason banks hire armies of consultants just to handle data mapping.

Poor Data Quality and Inconsistent Reference Data

Beyond structural differences, the quality of data itself is often questionable. Over the years, manual data entry, mergers and acquisitions, and system upgrades create duplication, missing lineage and incomplete records. Reference data — such as product codes, branch identifiers or customer segmentation — may exist in multiple versions across different systems. Without standardised reference data, it’s impossible to guarantee that a migrated record will be interpreted correctly in the new system.

When data quality issues arise, they cascade through the entire migration workflow. Consider a core banking migration where account balances are stored in different currencies or aggregated differently across systems. Unless this is addressed up front, even minor discrepancies can create significant mismatches after migration, leading to reconciliation efforts that take weeks or months.

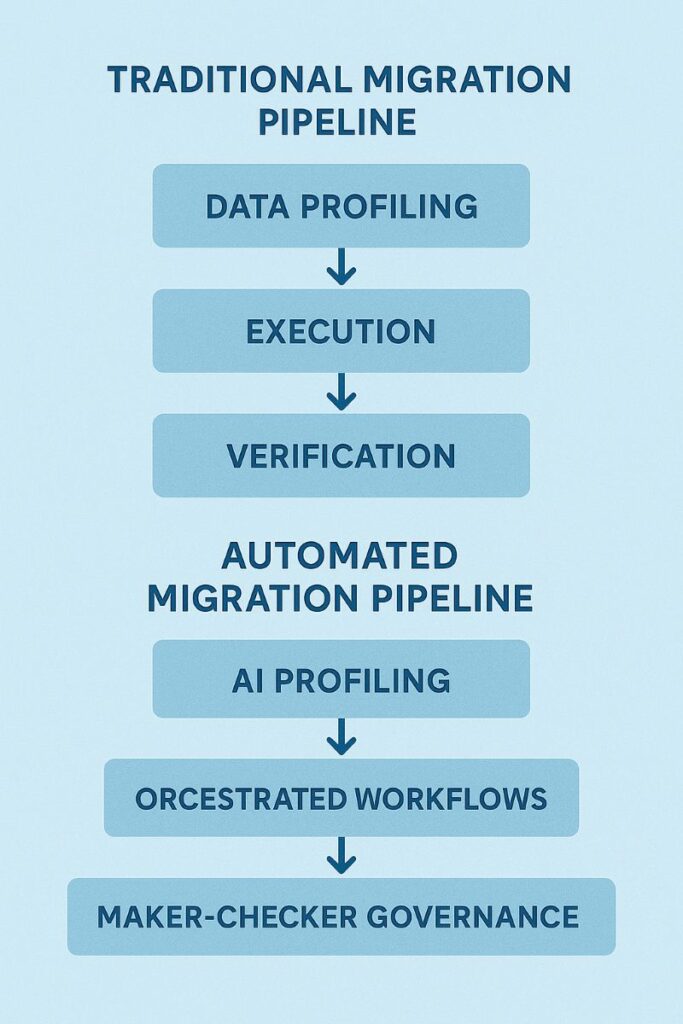

Brittle Pipelines and Manual Processes

Traditional migration methods rely heavily on custom ETL scripts that extract data from source systems, transform it into a canonical format and load it into the target platform. Because these scripts are often built quickly and without a deep understanding of the underlying data, they break easily when unexpected data exceptions occur. For example, if a field is null or contains an unexpected value, the entire pipeline may halt. These brittle pipelines require constant maintenance, diverting developers from delivering new features.

Compounding the problem is manual validation. In many banks, quality assurance teams rely on spreadsheets to reconcile data after migration. They manually compare records from old and new systems, create pivot tables to find discrepancies and email lists of errors back to developers. This reactive clean‑up process consumes enormous hours, introduces human error and exposes the bank to compliance risk. Regulators may demand evidence of migration quality — something a manual, spreadsheet‑driven process cannot provide at scale.

The Consequence: Operational and Reputational Risk

These technical challenges translate into significant business risk. Operationally, if accounts are migrated incorrectly, transactions can fail or be misreported. Customers may see wrong balances, failed payments or duplicate charges. Reputationally, any migration error damages trust, especially for banks dealing with sensitive financial data. Regulators may issue fines or restrict new product launches until issues are resolved. In short, data migration is not just an IT problem — it’s a strategic risk that must be managed at the highest levels of the organisation.

De‑Risking Through Automation – A New Paradigm for Data Migration

Reactive Migration vs. Automated, Policy‑Driven Transformation

CoreAI Integrate: Four Principles for Safe Migration

At Ennovision, we saw the need for a solution that could de‑risk migration at scale through automation, governance and transparency. That’s why we built CoreAI Integrate — an AI‑powered workbench designed specifically to make data migration faster and fundamentally safer. The platform is anchored on four core principles:

- AI‑Driven Data Profiling. Before any migration begins, CoreAI Integrate automatically scans source data to detect patterns, data types, anomalies and outliers. By understanding the shape and distribution of data up front, the platform generates accurate mappings and highlights quality issues early. This discovery phase ensures that migration pipelines are built on a foundation of data awareness, not guesswork.

- Orchestrated ETL Pipelines. Rather than bespoke scripts, CoreAI Integrate uses pre‑built connectors and configurable workflows. These orchestrated pipelines handle extraction, transformation and loading in a controlled sequence, ensuring that business rules are applied consistently and that failures are captured and remediated automatically. Pipelines run continuously and can be scaled across multiple environments.

- Maker‑Checker Governance. One of the biggest sources of risk in migration is uncontrolled change. CoreAI Integrate addresses this through a robust maker‑checker model that enforces segregation of duties. Data mappings, transformations and policies must be approved by authorised stakeholders before execution. Every change is versioned, with an audit trail that satisfies regulators and internal compliance teams.

- End‑to‑End Traceability. Regulators demand proof that data migration was accurate and complete. CoreAI Integrate provides full lineage from source to target, enabling teams to trace every data element through its journey. This traceability not only satisfies compliance requirements but also empowers business users to verify outcomes and drive continuous improvement.

From Big Bang Risk to Controlled Repeatability

By combining these principles, automated platforms like CoreAI Integrate shift migration from a high‑risk “big bang” event to a controlled, repeatable and testable process. Migration can be run in small batches, validated automatically and rolled back if issues arise. Because policies are codified and enforced consistently, there is little room for human error. This repeatability allows transformation leaders to report progress with confidence and to iterate faster.

The Role of AI and Machine Learning

While automation is the foundation, artificial intelligence extends migration reliability and speed even further. Machine learning models can identify complex data patterns that traditional rules might miss. For example, an AI model can detect cross‑field dependencies between customer records, automatically suggesting grouping or deduplication strategies. AI can also predict pipeline failures based on historical runs, enabling preemptive fixes. These capabilities will become even more important as banks adopt advanced analytics and real‑time decision engines.

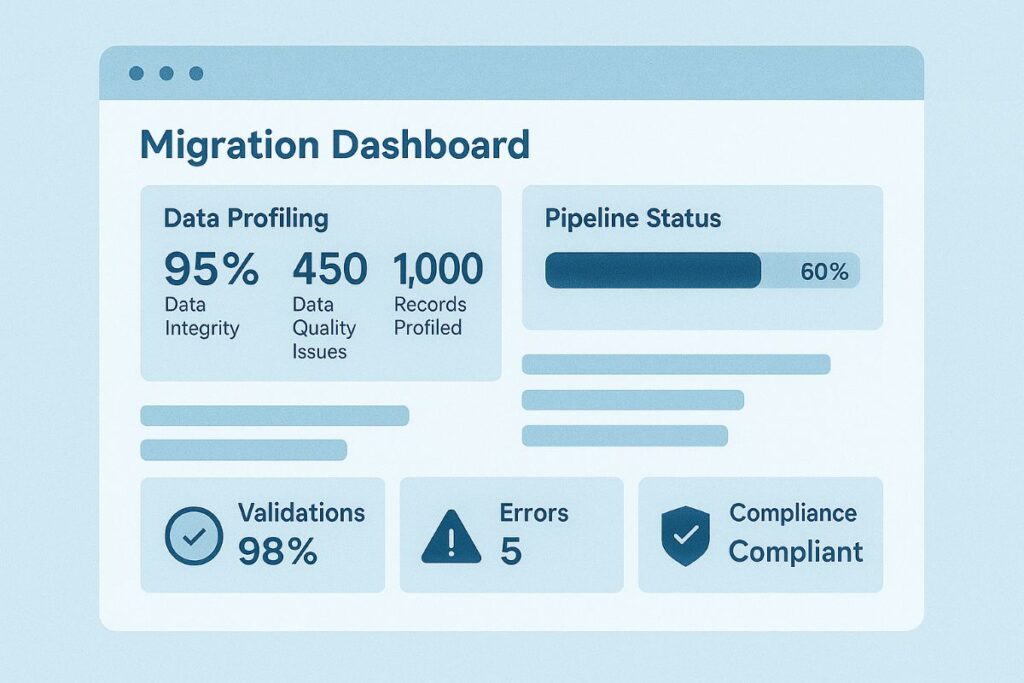

In our experience, AI‑driven profiling is particularly valuable during discovery. In one project, CoreAI Integrate analysed billions of records across 30 systems and identified that 15% of the customer addresses contained inconsistent postcode formats. Without automated profiling, such inconsistencies would have surfaced only after the migration, causing days of reconciliation work.

Lessons Learned from Global Transformation Programmes

Over years of leading data and AI transformation programmes across institutions of all sizes, we have distilled several patterns that underpin successful migrations. These lessons are drawn from both the failures and successes of banks in Asia, Europe and the Americas, and they inform how we design our tooling and advisory services.

Start with Discovery, Not Development

Don’t Over‑Rely on People for Quality Assurance

Manual validation is one of the biggest causes of delays and errors. While human expertise is necessary to define business rules, relying on people to reconcile every record is inefficient and risky. Instead, invest in automated validation frameworks. These frameworks run checks after each pipeline execution, compare results against expected thresholds and flag anomalies for review. Visual dashboards can show pass/fail rates, enabling teams to focus on the few exceptions that truly need manual intervention.

In our programmes, we embed automated tests as part of the migration pipelines. For example, if the rule states that every migrated loan must have a non‑null interest rate and a valid borrower ID, the pipeline automatically rejects any record that violates these conditions. Only those exceptions are sent to analysts. Over time, as the pipeline learns, the number of exceptions decreases dramatically.

Business Must Own Validation

Another lesson is that business must own validation. Too often, IT teams build migration scripts and sign off on success without consulting business stakeholders. This leads to mismatches between what was delivered and what the business expects. To avoid this, create a cross‑functional validation framework where domain experts define success criteria, review test results and sign off on migrated data. When business owners are accountable, the final platform is more likely to meet user needs.

Think Beyond the Cutover

Migration doesn’t end at the cutover. Once the new system is live, banks must continue to operate both old and new cores in parallel (for a transition period) while ensuring that incoming data flows remain consistent. They must also support post‑migration reconciliations, implement new analytics and maintain an evergreen migration pipeline for incremental changes. Thinking beyond go‑live ensures that the operational team is equipped to handle anomalies gracefully, avoiding disruptions to customer service.

Choose a Partner with Domain Expertise

Summary of Lessons: Discovery first; automation over manual QA; business‑owned validation; think beyond cutover; domain expertise matters.

Migration as a Strategic Enabler – Reframing the Conversation

Changing the Narrative: From Minimising Downtime to Maximising Traceability

When people talk about migration, they often frame it in terms of pain: “How do we minimise downtime?” But migration has the potential to unlock strategic advantage. By treating migration as a governance problem, banks can shift the narrative to maximising traceability and auditability. In other words, migration can be a catalyst for better data management. If you can orchestrate 20 pipelines intelligently and validate outcomes in real‑time with confidence, you have laid the foundation for continuous innovation.

Orchestrated Pipelines Enable Continuous Delivery

In a world of continuous delivery, the ability to migrate data seamlessly enables banks to add new services on top of existing cores. Rather than viewing migration as a one‑time event, treat it as an ongoing capability. When new products are launched — such as real‑time payments, open banking APIs or personalised lending — data flows must be extended or remapped. An orchestrated migration layer with automated policies allows these changes to be made without fear of breaking core processes.

Empowering Business Users with Real‑Time Validation

Traditional migration leaves business users in the dark until after go‑live. With automated pipelines and dashboards, business users can monitor key metrics during migration. If they see a drop in data quality or a surge in exceptions, they can collaborate with IT to refine policies. This transparency empowers business units to proactively manage change and reduces the friction often seen between IT and operations.

Building Organisational Confidence

Perhaps the most valuable outcome of reframing migration as a strategic enabler is building organisational confidence. When senior leaders see a clear plan for data migration, backed by automated governance and transparent reporting, they are more willing to support bold transformations. Teams that trust their migration process will move faster, accept less technical debt and have the courage to innovate.

Purpose‑Built Migration Platforms – The Case for CoreAI Integrate

Inflection Point: Why Banks Need a Dedicated Layer

The industry has reached an inflection point where core banking transformations cannot succeed without a dedicated migration layer. As banks increasingly adopt digital‑native platforms and cloud‑first strategies, they need a layer that sits between legacy systems and modern cores, orchestrating migration with intelligence, governance and speed. This layer must not only move data but also manage quality, enforce policies and provide transparency.

Legacy ETL tools or generic integration platforms often lack the context and governance required for core banking migration. They may handle data volume but not the nuance of regulatory classification or cross‑system relationships. A purpose‑built platform like CoreAI Integrate embeds these requirements from the ground up, reducing the need for custom code and lowering the risk of errors.

Features That Matter: Profiling, Pipelines, Governance and Traceability

We’ve already outlined the four principles of CoreAI Integrate. Let’s delve deeper into the features that differentiate a purpose‑built migration platform:

- Pre‑built Connectors for Core Systems. CoreAI Integrate includes connectors for common banking packages, mainframes and databases. These connectors understand native data structures, enabling rapid onboarding.

- Configurable Transformation Rules. Business users can define transformation rules through a graphical interface. Rules include logic for currency conversion, interest calculation, product mapping and more. Once defined, they are version controlled and stored as policies.

- Real‑Time Monitoring and Alerting. Dashboards display pipeline status, data quality metrics and exception queues. Alerting mechanisms notify teams when thresholds are crossed, enabling proactive intervention.

- Regulatory Compliance Modules. Migration policies can include regulatory constraints, such as anonymising personal data or mapping fields according to data localisation laws. This ensures compliance is embedded into the process rather than bolted on.

- Post‑Migration Tools. After cutover, the platform continues to monitor data flows, reconcile daily transactions and generate audit logs. Post‑migration analytics help identify opportunities for optimisation, such as archiving redundant data or improving schema design.

Integration with Ennovision’s Services

CoreAI Integrate is more than a stand‑alone tool; it sits within Ennovision’s broader ecosystem of services. Our teams leverage cloud engineering practices to deploy and scale migration pipelines on secure, resilient infrastructure. Our application engineering specialists build custom adapters when connecting to bespoke legacy systems. Our architecture consulting team ensures that migration strategies align with enterprise architecture standards and regulatory frameworks. And our AI‑powered data analytics experts help banks derive insights from migrated data to drive personalisation and product innovation.

If you’d like to learn more about how these services complement the platform, explore Ennovision’s offerings:

📎 Cloud engineering services – Cloud Engineering

📎 Application development and modernisation – Application Engineering

📎 Enterprise and solution architecture consulting – Architecture Consulting

📎 AI‑powered data analytics – AI‑Powered Data Analytics

Strategic Recommendations for Transformation Leaders

1. Elevate Migration to a Stand‑Alone Workstream

2. Invest in Discovery and Data Profiling

3. Integrate Governance Early

4. Think Holistically About Post‑Migration

5. Make Automation the Default

Executive Summary: Migration is not an IT chore but a strategic capability. Elevate it, invest in discovery, embed governance, plan beyond go‑live and automate everything.

Looking Ahead – Migration as a Competitive Advantage

The Composable Bank

Continuous Modernisation

Trust and Transparency

A Platform for Innovation

Conclusion – Empowering Banks to Transform Fearlessly

Data migration is the silent make‑or‑break moment in any core banking transformation. It is a risk not because it’s complicated but because it has historically been treated as an afterthought. We have learned that ignoring migration risk can derail even the most ambitious programmes. But we’ve also learned that automation and policy‑driven governance change everything. By investing in dedicated tooling like CoreAI Integrate, adopting AI‑driven profiling, implementing maker‑checker controls and insisting on end‑to‑end traceability, banks can turn migration from a bottleneck into a source of competitive advantage.

At Ennovision, we believe every bank should be empowered to move forward without fear. That belief drives our investment in AI, automation, cloud engineering and data architecture. We invite you to reframe your migration journey — not as a risky hurdle but as a strategic enabler of innovation. When you de‑risk your data journey, you unlock a world of possibilities: faster product launches, deeper customer insights and unwavering regulatory compliance.

Final Thought: Safe, automated migration is not just a project milestone. It is the foundation on which the next decade of banking innovation will be built. Embrace it, and your organisation will be ready for whatever the future holds.